Copy Link

Copy Link

Share

to X

Share

to X

Share

to Facebook

Share

to Facebook

Share

to LinkedIn

Share

to LinkedIn

Share

on Email

Share

on Email

Most parents don't need more tips about teaching kids about money. They need a system. Something with shape. Something a 5-year-old can hold in her hands and a parent can stick to without remembering 14 different rules.

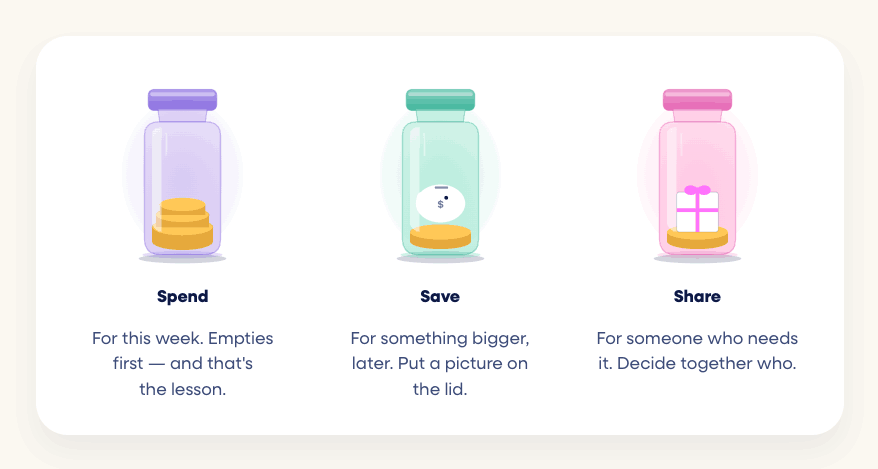

The spend, save, share method is that system. Three jars, three categories, one weekly ritual. It has been used by families for as long as there have been coins, and it shows up in almost every culture's folk wisdom about money. The reason it has survived isn't because it's clever. It's because it works.

This guide is the complete version for the 4 to 7 age window: what the method actually does, how to set it up at home this weekend, what splits make sense at each age, what to do at the predictable hard moments, and how it connects to deeper values like generosity and shared resources. If you've read our parent's playbook on how to teach kids about money, this article is the framework deep-dive.

The short version

Money management for kids at ages 4 to 7 is best taught through the spend, save, share method: three clear jars, a small weekly deposit, and a short conversation about how to split it. The skills this builds (deciding between now and later, choosing what to share, setting a small goal and watching progress toward it) are the foundational money management skills for kids in this age window. The percentages matter far less than the ritual; what makes the method work is consistency and visibility, not math.

What the spend, save, share method actually does

At first glance, three jars looks like a budgeting trick for children. It isn't. Or it isn't only that.

The method does three things at once, and that's why it's stuck around:

It makes the invisible visible. Money for a 5-year-old is an idea floating around in the air. Phones tap, cards swipe, things appear. Three labelled jars sitting on a shelf in her room turn that idea into something physical: this much for now, this much for later, this much for someone else. The jars are how the concept enters the body.

It teaches that money is a set of choices, not a single thing. Adults forget how strange this is to a child. Money isn't one thing you spend; it's a thing that can be split, allocated, prioritised, and shaped. Once a child has divided a single dollar three ways and felt that each portion has a different job, she has the foundation for almost every adult financial concept that follows.

It builds the habit before the math. This is the part most guides miss. The method works at age 4 long before any child can do the math of percentages. The habit of dividing money is what matters. The percentages come later, naturally, once the habit is in place. Parents who wait until their child is "old enough to understand the math" wait too long. The math is the easy part. The habit is the hard part.

Research from the University of Cambridge by Dr. David Whitebread found that money habits, including the ability to plan, divide, and delay, are largely set by age 7. The three-jar system is one of the few frameworks that is genuinely teachable inside that window, because it works at the level of physical experience rather than abstract reasoning.

A quick note on "share" vs. "give"

Some versions of this method use "give" as the third jar. We use "share" for a reason worth naming.

"Give" is a transactional word. You give money away and it's gone. For young children, this can feel like a small loss, which is not the feeling we want to attach to generosity. "Share" reframes the same act as a contribution. Sharing your coins with someone who needs them more, or with a group that's building something for everyone, isn't a loss. It's a way of making your money do something it can't do alone in a jar.

This isn't just semantics. Children pick up emotional tone fast. The word you use for the third jar shapes the feeling she has about putting money in it. "Share" feels lighter, warmer, and more durable than "give."

If you've already been using "give" with your child and it's working, don't switch. The word matters less than the practice. But if you're starting fresh, "share" is the version we'd recommend.

How to set up the three jars at home

This whole system can be set up in 30 minutes, and most of that is finding three containers — a quick trip to a shop, or just three jars from around your home.

What you need

- Three clear containers. Glass jars, plastic boxes, even plastic cups. The clarity matters more than the container.

- Three labels (or a marker). Label them Spend, Save, and Share.

- A starting deposit. Whatever loose change or small bills you have on hand. Even $3 is enough.

- A spot. Somewhere visible. The kitchen counter, your child's room, a shelf they pass every morning.

Optional but useful: printable jar labels (there are dozens of free templates online, or a marker works), and a single sheet of paper taped near the jars to track the weekly deposit. Some families also like a simple money management for kids worksheet to record the weekly split; that's not necessary, but if your child responds well to writing things down, it adds a small layer of ritual.

The setup conversation

Sit on the floor with your child. Bring the three empty jars. Hand her the markers.

Explain it in language she'll get. Try something like:

"This jar is for now. When you want something small and you want it soon, this is the jar you reach for. This jar is for later. When there's something you really want but it's bigger, you put coins in this one and watch them stack up. This jar is for somebody else. Either to help someone who needs it more than us, or to put money toward something we all want to do together. Three jars. Three jobs."

Then let her decorate them. Stickers, glitter, drawings. The more she owns the jars, the more she'll engage with them. This is not a side activity. It's the most important part of the setup.

The first deposit

Sit with her and split the starting amount. Don't tell her the right way; ask her what she thinks. "You have these coins. How do you want to split them between the three jars?" Whatever she says, work with it. If she puts everything in the spend jar, gently nudge: "What about a little in save? What about share?" But let her make the final call.

The first split is almost never optimal. That's fine. The point is that she made it.

The weekly ritual

This is the engine of the whole system. Pick a day and a moment that's already part of your week. Sunday after breakfast. Friday before bedtime. The Saturday morning grocery run.

Each week, hand her her allowance (or whatever the regular deposit is). Together, count it out and decide how it splits across the three jars. Same ritual every time. Same jars. Same conversation.

The ritual matters because the lesson isn't carried in any single deposit; it's carried in the repetition. After a month of splitting money weekly, your child has internalised the structure. After three months, she does it without prompting. After a year, the habit is so deeply embedded she'll do it as a teenager without remembering where she learned it.

A six-page parent's companion to Scooter Park Fun! The four money moments your child will play through, the exact question to ask at each one, and three quick activities to try after the screen goes off. Free, no email needed.

Or open Scooter Park Fun! in the Nurture app to play it together tonight.

Age-appropriate splits and percentages

Parents often ask what percentage should go in each jar. The honest answer is: less than you think the percentages matter, and more than you think the choosing of the percentages matters.

Here's a grounded version by age.

Ages 4–5: equal thirds, simply

Don't introduce percentages. Don't introduce math. Just three coins in each jar. The lesson at this age is that money divides three ways. That's it. Equal thirds is the easiest version to set up and the easiest to feel.

If your child wants to put more in one jar than another, follow her lead the first few times. Once the habit is in place, you can start to gently coach. "Let's put one in each first, then see what's left."

Ages 5–6: the 50-25-25 split, with conversation

Now the math starts to be reachable, but only just. A simple version: half goes to spend, a quarter to save, a quarter to share. With a $4 weekly allowance, that's $2 spend, $1 save, $1 share. Round numbers that a 6-year-old can do in her head.

Don't fix this in stone. Each week, ask: "How do you want to split it this week?" Sometimes the save jar is empty and she wants to top it up. Sometimes she wants to share more because she has a specific person in mind. The percentages are a default; the conversation is the lesson.

Ages 6–7: the 50-30-20 split, with reasoning

At this age, the standard adult budgeting starting point starts to make sense: 50% spend, 30% save, 20% share. Use real percentages now. Talk through why. "Save is bigger now because the things you want are bigger. Share stays as a piece of every dollar because sharing isn't about extra; it's about how you treat money."

This is also the age where she might want to introduce a fourth jar (a long-term save jar for something six months out, alongside the regular save jar for things this month). Let her. The system is meant to flex.

A caveat about the numbers

The percentages are training wheels. They're a starting point, not a rule. The whole point of the system at this age is to teach the act of dividing, not to enforce a specific ratio. A child who splits her money 70-20-10 every week and can articulate why has learned more than a child who splits 50-30-20 because a parent told her to.

The "I want to spend everything" moment

This will happen, and how you handle it shapes everything that follows.

Within the first three months of starting the system, your child will look at her spend jar and want to also empty her save jar to buy something. Or she'll look at her share jar and want to "move that money to spend, just this once." Or she'll look at a new toy at the store and ask if she can dump the whole structure for it.

The instinct as a parent is to refuse. Don't.

The instinct as a parent is also to lecture. Definitely don't.

What to do instead: hand the decision back. "That's your money. You can do that if you want. But that means the [save goal] doesn't happen this month. And the share jar is empty when we go to do the thing we'd planned with it. Is that the trade you want to make?"

Then wait. Let her think.

If she goes through with it, she'll feel the consequence later. The save goal won't happen. The share moment will come up empty. Those feelings are the lesson, and they don't need to be reinforced with a lecture from you.

If she pulls back, that's a win, and it's a win she earned by thinking. Just notice it out loud. "You stuck with the plan. That was your choice."

The whole system depends on the money being hers, the decisions being hers, and the consequences being hers. Parents who turn the jars into rules they enforce miss the entire mechanism. The jars only teach if the choices inside them are real.

How "Scooter Park Fun!" teaches the spend, save, share method through play

There's a piece of the spend, save, share framework that's hard to teach through jars alone: the share part, specifically the version of sharing that's about pooling resources to build something everyone can use.

This is the concept at the heart of Nurture's Scooter Park Fun!. In the story, Chirp wants to build a scooter park, but the pieces cost more coins than she has on her own. Fizz suggests pooling their Fluffle Coins together. Across the adventure, children make spending decisions (which pieces to buy first), saving decisions (which coins to hold back for later in case something better comes up), and sharing decisions (pooling with Fizz to afford what neither could afford alone).

What the adventure does that jars alone can't: it shows the result of pooled sharing. A scooter park visibly takes shape across the play session because resources were combined. Children playing the adventure aren't told that sharing builds bigger things than spending alone. They watch it happen. That single experience plants a seed your everyday three-jar system keeps watering.

A specific moment from the adventure worth knowing about: there's a point where Chirp could choose to spend all her coins on a piece she wants alone, or to combine with Fizz on something bigger. The game lets her make either choice. The consequence plays out in the scooter park. That's the spend, save, share method made visible at the moment of decision, in a way no jar at home can replicate. It's also why parents using the three jars at home and playing Scooter Park Fun! together often find their conversations sharpen: the abstract framework gains a concrete example her brain can return to.

The share jar deserves its own moment

Most three-jar guides treat the share jar as the smallest, simplest of the three. It isn't. It's quietly the most powerful one in the long run, and it deserves more thought than it usually gets.

The share jar teaches two things that the other jars don't:

That money can do work in the world. A child who watches her share jar fund a meal for a family in need, or buy a book donated to a school, or contribute to a pet shelter has had a financial experience most adults never explicitly have. Money has stopped being purely about acquisition for her. It has become a tool for action.

That she has agency in a community. The share jar is small, but it's hers, and she gets to decide what it does. That feeling (I have something to give, and what I do with it matters) is the foundation of civic identity. It also makes future conversations about taxes, charities, and shared public goods land far more easily than they otherwise would.

A few practical notes on the share jar specifically:

- Let her choose the cause. This isn't a parent decision. Sometimes the choice will be wonderful (an animal shelter, a sick friend). Sometimes it will be weirdly specific ("I want to give it to the lady at the coffee shop"). Both are fine. The choosing is the lesson.

- Cash it in regularly. Don't let the share jar sit untouched for a year. Once it's at a meaningful amount (whatever that is in your family), spend it on the thing she chose, with her, where she can see it happen.

- Tie it to family rituals. Some families empty the share jar once a year (around the holidays). Others do it monthly. Either works. What doesn't work is letting it become an abstract pile of coins. The share jar has to do something visible, or the meaning evaporates.

- It's allowed to be smaller. If she wants to put 10% in share and 90% elsewhere, that's fine. The principle is that some piece of every dollar gets allocated to others. The size matters less than the practice.

Connecting money to values

Here's a piece of the spend, save, share method that's easy to overlook: it isn't actually a financial framework. It's a values framework with money attached.

When a child decides what goes in her share jar, she's deciding what kind of person she wants to be. When she chooses to save for something instead of spend now, she's practising a version of herself she might be later. When she gives her spend jar to the toy and feels the empty jar afterward, she's learning something about what she values and what she doesn't.

This is why the method outlasts the specific dollar amounts. The percentages will change as she gets older. The jars will eventually become an app. The structure will eventually be invisible. But the underlying habit (some of what I have is for now, some is for later, some is for others) is a values habit, not a financial one. Build it well at 5 and it shapes how she handles a paycheck at 25.

This is also why the method works across very different family financial situations. The percentages don't need to be large. The amounts don't need to be much. A child saving $1 a week and sharing $0.50 has had the same formative experience as a child saving $20 a week and sharing $10. The structure does the work. The structure is what you're teaching.

Your week-one money management plan

Lightest possible starting version:

This weekend: Buy or find three clear containers. Label them. Sit with your child and let her decorate them. Make the first deposit together. Don't over-think the split; let her lead with gentle coaching.

This week: Pick a weekly time and a weekly amount. Stick with it. Make the second deposit at the same time, same place, same way.

This month: Don't change the system. Don't add complexity. Just keep showing up. By week four, the ritual will have its own gravity, and the lesson will be working without your active management.

That's it. Three jars, three deposits, one ritual. The hardest part is not over-complicating it.

Practice this with your child

Nurture's Scooter Park Fun! adventure is designed for ages 4–7 and teaches the spend, save, share method through an interactive scooter park story. Kids make real decisions about spending, saving, and pooling resources using Fluffle Coins, in a story that makes the framework feel lived rather than explained.

Frequently asked questions

What is the spend, save, share method for kids?

The spend, save, share method (sometimes called the three-jar system) is a simple framework for teaching children to divide their money three ways: a portion to spend now on small things they want, a portion to save toward larger goals, and a portion to share with others or contribute to a group goal. It works because it turns the abstract concept of "managing money" into a physical, visible, weekly ritual that a child as young as 4 can engage with.

At what age should kids start using the three-jar system?

Children can start with a simple version at age 4, when they begin to grasp that money comes in pieces that can be divided. At this age, equal thirds is enough; percentages and math come later. By ages 6 to 7, more nuanced splits (like 50% spend, 30% save, 20% share) become realistic. The earlier the habit of dividing is established, the more durable it tends to be.

What percentages should go in each jar?

There's no universally correct split. For ages 4 to 5, equal thirds is simplest and most effective. For ages 5 to 6, a 50-25-25 split (spend, save, share) is a reasonable starting point. For ages 6 to 7, the 50-30-20 split commonly used in adult budgeting can be introduced. More important than any specific ratio is that the child participates in choosing the split each week and understands why each jar matters.

Why is it called "share" instead of "give"?

Either word works, but "share" tends to work better with young children. "Give" carries a connotation of loss (something leaves and is gone), which can quietly attach a negative feeling to generosity. "Share" reframes the same act as a contribution to something bigger (a community need, a group goal, a person who needs the resource more). Children pick up emotional tone fast, and the word shapes the feeling. If "give" is already working for your family, stay with it. If you're starting fresh, "share" is the recommended version.

What if my child wants to spend everything from all three jars?

This is one of the most predictable moments in the method, and it's also one of the most important. Don't refuse and don't lecture. Hand the decision back: "That's your money. You can do that, but here's what it means for the goals you set." Then let her choose. Either she pulls back (a win she earned) or she goes ahead and feels the consequence (also a lesson). The jars only teach if the choices inside them are real and reversible.

How much allowance should my child get for the three-jar system to work?

The system works at almost any allowance amount. A common rule of thumb is roughly $1 per year of age per week ($5 for a 5-year-old, $7 for a 7-year-old). The exact amount matters less than the consistency. A $3 weekly allowance split three ways teaches more than a $30 monthly lump sum with no structure. Small, regular, and predictable beats large and sporadic every time.

How is the three-jar system different from a piggy bank?

A piggy bank teaches one concept: saving. The three-jar system teaches three at once: spending wisely, saving toward goals, and sharing with others. A piggy bank also hides progress (you can't see how much is in it), which works against the visual feedback young children need. The three-jar system uses clear containers so the contents of each jar are always visible, making the abstract idea of money management tangible at every glance.

What are the most important money management skills for kids?

For ages 4 to 7, four skills matter more than any others. First, dividing money rather than treating it as one undifferentiated pile. Second, setting a small visible goal and watching progress toward it. Third, making a trade-off out loud (choosing this over that). Fourth, noticing the feeling that follows a money decision (regret, satisfaction, anticipation) and naming it. These four skills are the foundation that every later money management skill builds on. Percentages, budgeting apps, and investment concepts can wait.

What are some money management games and activities for kids?

Money management games and activities for kids ages 4 to 7 work best when they recreate real decisions in a low-stakes setting. The pretend store at home (with pantry items and sticky-note price tags) is the strongest free activity. Monopoly Junior and The Allowance Game are reliable structured options. For digital play, Nurture's Scooter Park Fun! adventure is purpose-built for this age window. See our guide to financial literacy games for kids for a full review of what works and what to skip.

Are there free money management resources for parents?

Yes. The U.S. Federal Deposit Insurance Corporation publishes Money Smart for Young People, a free, age-graded financial education curriculum that parents and teachers can download. For ages 4 to 7 specifically, the early modules pair well with the three-jar system at home. The U.S. Consumer Financial Protection Bureau also maintains a free library of youth financial education activities, age-tagged and printable.